Structured funds

Key Messages:

- Unlike conventional funds, which achieve their objectives through direct investment in stocks, bonds, etc, structured funds do so through substantial investment in derivatives.

- For example, if the investment return of a structured fund is linked to an index, the fund may invest in a swap to simulate the performance of that index. This will subject the fund to default risk of the swap counterparty. While such a risk may be reduced by collateral provided by the counterparty, it may be difficult to enforce or liquidate the collateral.

- Always check out the key facts in the fund's offering documents. In addition, ask the selling intermediary to thoroughly explain the fund structure and its investment details, and why a structured fund is suitable for you, having regard to your financial situation, investment experience and investment objectives.

A structured fund is a collective investment scheme where the management company seeks to achieve its investment objectives primarily through investment in or use of financial derivative instruments (for example, swap, repo or access products). A structured fund is usually passively managed and some may offer payouts if the pre-determined conditions are met. Some of the guaranteed funds available in the market are also structured funds.

A structured fund is a collective investment scheme where the management company seeks to achieve its investment objectives primarily through investment in or use of financial derivative instruments (for example, swap, repo or access products). A structured fund is usually passively managed and some may offer payouts if the pre-determined conditions are met. Some of the guaranteed funds available in the market are also structured funds.

A typical structured fund enters into an over-the-counter (OTC) index-linked swap (see explanation below) with a financial institution that acts as the swap counterparty. A swap is an investment instrument which enables two parties to exchange their assets or cash flows. A swap can be either funded or unfunded. Through the swap, the fund receives the investment returns based on the performance of the underlying index.

Under the counterparty exposure limitation requirements imposed by the SFC and respective home jurisdictions at the fund's place of incorporation, the manager of the fund will aim to limit the fund's daily risk exposure to the swap counterparty to no more than 10% of the fund's net asset value (NAV). In case the fund's gross risk exposure to the swap counterparty exceeds 10% of its NAV, the swap counterparty will have to provide collateral so that the fund's risk exposure to the counterparty is reduced to 10% or below of the fund's NAV. The collateral must also meet the eligibility requirements imposed by the SFC and relevant home jurisdiction and will be marked-to-market at the end of each trading day.

The underlying index invested in by a typical structured fund may be a proprietary index (see below).

What is a proprietary index?

A proprietary index is an index that has not been publicly launched in the market. It is developed to track the performance of an underlying asset class (equity, bond, commodities, etc.) and market (developed, emerging, etc.), and owned by a financial institution or a data vendor called an index sponsor, who continues to own and manage the index on an on-going basis. A proprietary index, for instance, can be developed to replicate the performance of a hedge fund.

A third party index, on the other hand, is an index that has been publicly launched in the market. Hang Seng Index is an example of a third party index.

Structured fund vs non-structured fund

The table below sets out a comparison of a conventional non-structured fund and a typical structured fund investing in an index-linked swap:

| Non-structured fund that does not invest in derivatives | Typical structured fund investing in an index-linked swap | |

|---|---|---|

| Investment | Buys bonds and/or stocks directly | Gains exposure to an index through a swap |

| Derivative exposure | None | Yes - swap |

| Counterparty exposure | Issuer of invested bonds and/or stocks | Swap counterparty |

| Assets | Owns the bonds and/or stocks outright | No assets (in the case of a funded swap) or a portfolio of securities as agreed with the swap counterparty (in the case of an unfunded swap). In the case of a funded swap, the custodian can make claim for collateral on behalf of the fund if the swap counterparty is insolvent |

| Liquidity concern | Liquidity of bond and/or stocks bought | Liquidity of swap may be limited |

Illustration

The following diagrams illustrate the operation of typical structured funds investing in equity-linked swaps.

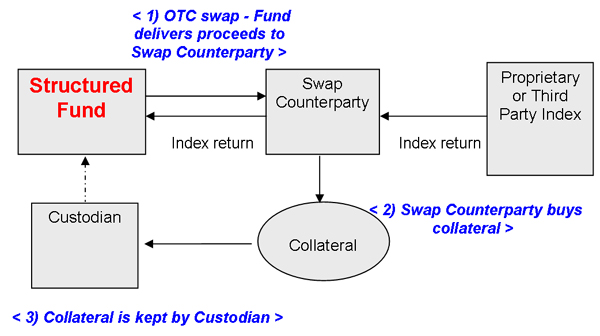

Funded swap

In a funded swap, the fund delivers the net proceeds from its subscriptions to the swap counterparty and will receive a return if the underlying index moves in the direction agreed. The fund's exposure to the swap counterparty will be collateralized up to at least 90% by a pool of securities, which will be delivered by the swap counterparty and deposited into an account maintained by the custodian and pledged in favor of the fund.

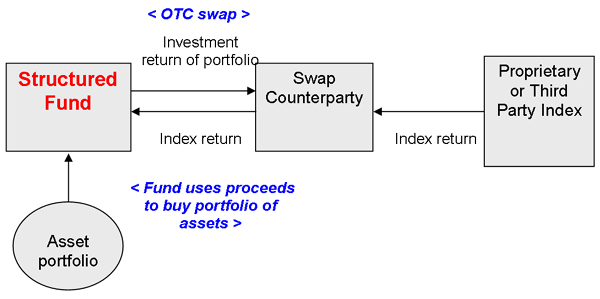

Unfunded swap

In an unfunded swap, the fund uses the net proceeds from its subscriptions to purchase a portfolio of securities. The fund then enters into an OTC swap and uses the returns generated by the portfolio of securities to exchange for the returns of the underlying index with the swap counterparty.

For both funded and unfunded swap structures, according to the counterparty exposure limitation requirements, the net counterparty exposure should be managed to no more than 10% of the NAV of the fund. If the fund's risk exposure exceeds the 10% threshold after the determination of its NAV at the end of a particular dealing day, the swap counterparty will have to put up additional collateral to reduce the counterparty exposure to below 10% of the fund's NAV. The additional collateral or asset portfolio (as the case may be) is usually not the constituent stocks of the underlying index of the OTC swap.

However, even though the fund can liquidate the collateral or asset portfolio of the fund if the swap counterparty defaults, the market value of such collateral or asset portfolio may have dropped substantially at the time of liquidation.

Major risks

1. Default risk of the swap counterparty: If the swap counterparty fails to perform its obligations under the swap, the fund may not be able to achieve its investment objectives and you may then suffer significant losses. In the event of a default of the swap counterparty and there is no new counterparty acceptable to the management company, the fund may be terminated and you will be fully exposed to the market risk of the value of the collateral / asset portfolio (as the case may be) and suffer losses.

2. Market risks: The value of the investment may rise or fall as a result of the performance of the underlying index. An underlying index tracking a market with limited access may be more volatile. If the index performs badly, the NAV of the fund may fall below the initial purchase price of the fund. You are also exposed to the economic, political, regulatory, currency, legal and other risks of a specific market the index is tracking.

3. Reliance on a single counterparty/business group: In some structures, the parties involved in the transaction (for instance, the fund management company, the swap counterparty and the index sponsor) may be different operational divisions belonging to the same legal entity. In other structures, these parties may be different legal entities belonging to the same group. You should consider if you are comfortable with the concentration risks involved.

4. Conflict of interests: As the parties involved could be the same legal entity or different legal entities belonging to the same group, there may be an issue of conflict of interests.

5. Enforceability of collateral: Be aware that often the enforcement of the collateral may involve cross-border jurisdictions and the interpretation of foreign law, which could lead to a delay or other difficulties in the enforcement or liquidation of the collateral.

6. Transparency of underlying index: For structured fund which tracks the performances of a proprietary index, bear in mind that information about the proprietary index, such as daily fixing and methodology of computation, may not be as readily available or as transparent as a third party index. Ask yourself - are you comfortable with the level of transparency and the availability of information about such an index?

To make an informed investment decision, always check out the important facts in the fund's offering document to thoroughly understand the structure of the fund and the investment details, especially information about the index, the investment strategy, the collateral arrangement, the swap counterparty and information about all the other parties involved and their relationships.

Also, consult your professional advisors to get a better understanding. Do not buy the product unless the intermediary who sells it to you has advised you that it is suitable for you and has explained why, including how it would be consistent with your investment objectives.